The Lobito Corridor

Reimagining Central African Logistics

Updated March 4, 2026

Central Africa sits on some of the most valuable mineral resources on earth. The DRC’s copper belt, cobalt deposits, and emerging lithium fields are not peripheral commodities in the global energy transition. They are foundational to it. Every electric vehicle battery, every offshore wind turbine, every grid-scale energy storage system requires materials that exist in extraordinary concentration in a relatively small geographic area straddling the DRC and Zambia. The world needs these minerals. The companies building clean energy infrastructure are prepared to pay for them. The governments of the DRC and Zambia are eager to export them.

The obstacle is logistics. Moving a tonne of copper concentrate from Katanga to a seaport currently requires navigating some of the worst road infrastructure, most congested border crossings, and most unpredictable transit times of any mining jurisdiction in the world. The cost penalty imposed by this infrastructure deficit is not a minor friction. It is a structural drag on the competitiveness of Central African mining that costs the region billions of dollars in foregone export revenue annually and deters the downstream processing investment that would generate far greater value than raw mineral export alone.

The Lobito Corridor is the most serious attempt in a generation to address this deficit at scale, with sovereign-backed financing, a long-term private concession structure, and geopolitical urgency that is translating commitment into construction.

KEY TAKEAWAYS

- The Lobito Corridor is the centrepiece of the US-backed Lobito Trans-African Corridor initiative, announced at the G7 Summit in 2023, and represents the most significant Western infrastructure commitment to Central Africa in decades, directly competing with Chinese Belt and Road investments in the region.

- The DRC holds an estimated 70 percent of the world’s cobalt reserves and significant deposits of copper, lithium, and rare earth elements that are critical to global electric vehicle and clean energy technology supply chains, making the corridor a strategic minerals access route of global importance.

- Current logistics costs for moving a container from the Katanga mining province of the DRC to an export port are among the highest in the world, estimated at two to three times the equivalent cost in comparable mining jurisdictions in Chile or Australia, and reducing this cost is the primary economic value proposition of the corridor.

- The corridor’s development is structured around a public-private partnership model in which the Lobito Atlantic Railway consortium (comprising Trafigura, Mota-Engil, and Vecturis) holds a 30-year concession for the Angolan rail section, with separate financing structures being assembled for the DRC and Zambia extensions.

- Beyond minerals logistics, the corridor creates the infrastructure backbone for agricultural trade, manufactured goods distribution, and regional economic integration across one of the most logistics-constrained zones of the African continent.

DEFINITION

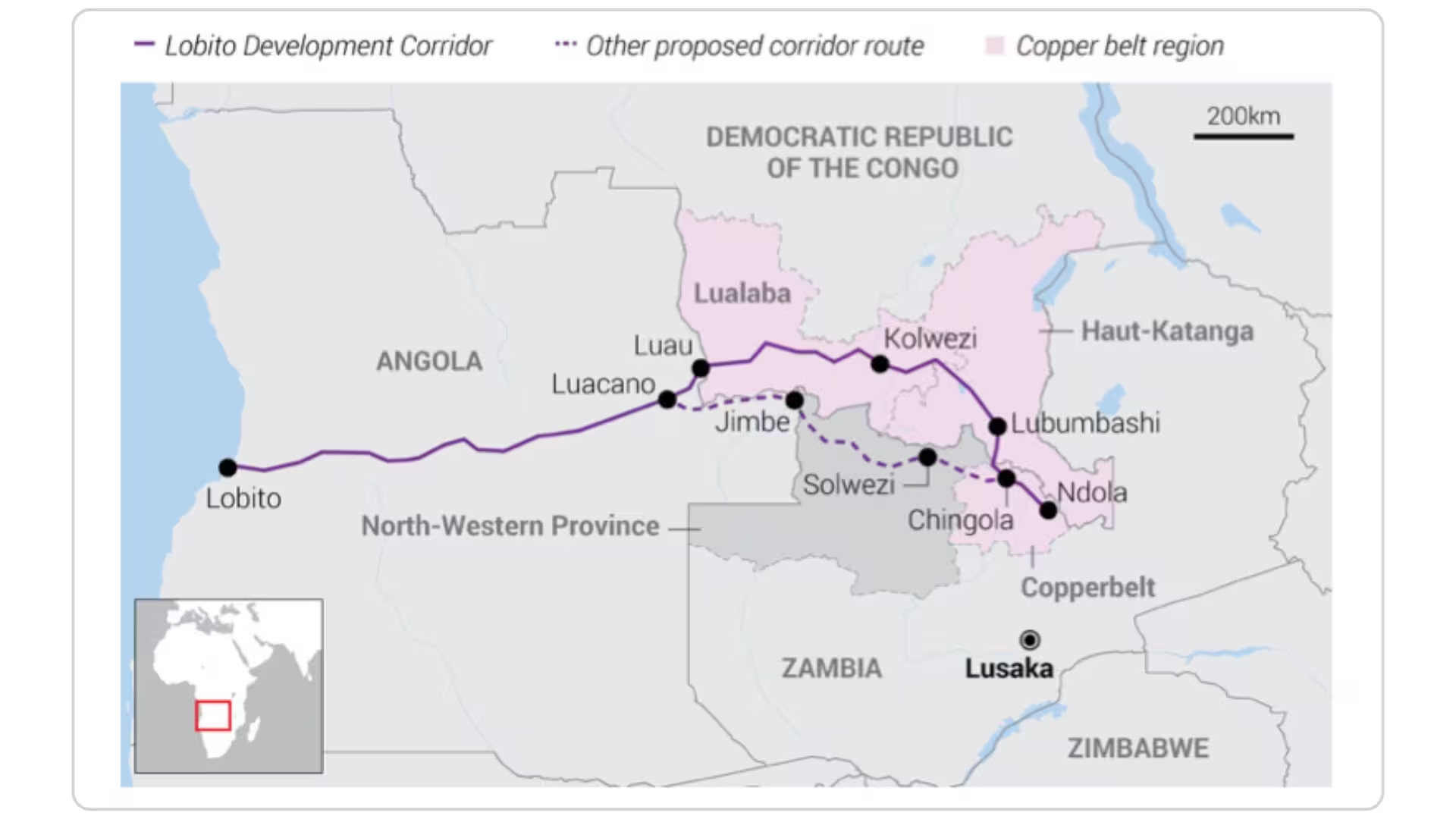

The Lobito Corridor refers to the approximately 1,300 kilometre rail and multimodal logistics route connecting the Atlantic port of Lobito in Angola through the Benguela Railway to the copper and cobalt mining districts of the Democratic Republic of Congo (DRC) and the copper belt of Zambia. In its extended conception, the corridor links to Tanzania’s port of Dar es Salaam on the Indian Ocean, creating the potential for a trans-continental freight route across Central and Southern Africa.

The corridor is a trade corridor in the formal infrastructure sense: a coordinated system of rail, road, port, border crossing, and logistics node investments designed not merely to move freight from point A to point B, but to catalyse economic development along its entire length by reducing the cost and time of moving goods between production zones, processing centres, and export terminals.

Table of Content

The Lobito Corridor: Reimagining Central African Logistics

This article is in BOH Infrastructure’s Infrastructure and Trade Corridors series. The full series establishes that physical connectivity is the single largest multiplier of AfCFTA value, and that the perception of African infrastructure risk consistently overstates the actual execution record. This briefing focuses on the specific corridors, port assets, and financing instruments that are closing the gap between ambition and delivery.

The Geopolitical Context

Why This Corridor, Why Now

The Lobito Corridor did not emerge from a development planning vacuum. Its acceleration from long-discussed aspiration to funded project with active construction is the direct product of the intensifying competition between the United States and China for influence over critical mineral supply chains in Africa.

China’s position in Central African infrastructure is longstanding and substantial. Chinese state-owned enterprises have financed and built roads, railways, hospitals, and government buildings across the DRC and Zambia over the past two decades, typically through resource-backed loan structures in which infrastructure financing is repaid through preferential access to mineral exports. The Sicomines copper-cobalt joint venture in the DRC, which exchanged mineral rights for infrastructure investment commitments, is the most discussed but far from the only example of this model across the region.

The US response, formalised through the Partnership for Global Infrastructure and Investment (PGII) announced at the 2022 G7 Summit and then specifically applied to the Lobito Corridor at the 2023 G7 Summit, represents a deliberate attempt to offer an alternative model: transparent concession structures, private sector financing complemented by development finance from the US International Development Finance Corporation (DFC) and the Export-Import Bank, and a logistics infrastructure focus rather than a resource extraction focus.

The DFC has committed over USD 550 million in financing to the Lobito Corridor project, with additional commitments from the European Union’s Global Gateway initiative and the African Development Bank. The EU’s involvement reflects European industrial exposure to the same critical mineral supply chain risk: European electric vehicle manufacturers are acutely aware that cobalt and copper supply chain concentration in a logistics-constrained region represents a strategic vulnerability.

For investors, the geopolitical backing of the corridor is not just an interesting contextual fact. It materially changes the risk profile of corridor-linked investments. Projects embedded in a geopolitically prioritised infrastructure programme are significantly less likely to face financing withdrawal, contract renegotiation, or regulatory disruption than equivalent projects in the absence of such backing. Sovereign and DFI support provides a form of political risk insurance that the commercial insurance market cannot easily replicate.

The Benguela Railway and the Angolan Section

The backbone of the Lobito Corridor is the Benguela Railway (CFB), which runs 1,344 kilometres from the port of Lobito on Angola’s Atlantic coast eastward to the DRC border at Luau. The railway was originally built by the British in the early twentieth century to serve the Katanga copper belt, and for decades it was one of the most important freight routes in Central Africa. The Angolan civil war, which lasted from 1975 to 2002, destroyed large sections of the track infrastructure and brought traffic to a halt for a generation.

The railway was partially rehabilitated by a Chinese state-owned enterprise between 2006 and 2015, restoring basic operational capacity on the Angolan section. The current phase of development, under the 30-year concession awarded to the Lobito Atlantic Railway consortium, is transforming the railway from a partially functional line to a modern freight corridor capable of handling the volumes that DRC and Zambian mining export demand requires.

The consortium partners bring complementary capabilities to the concession. Trafigura, one of the world’s largest commodity trading firms, brings guaranteed cargo volumes from its DRC and Zambian mining interests, providing the revenue anchor that makes the concession economics work. Mota-Engil, the Portuguese engineering and construction group with deep experience in African infrastructure, brings project execution capability. Vecturis, a Belgian rail operations specialist with existing African railway management experience, brings operational management expertise.

The Lobito port itself is undergoing parallel development. Currently handling general cargo and some bulk commodity shipments, the port requires expansion of its deep-water berth capacity, installation of modern bulk handling equipment for copper concentrate and other mineral exports, and development of logistics zones adjacent to the port for warehousing and value-added processing. The port expansion is being financed separately from the rail concession, with a combination of Angolan state resources and international development finance.

The DRC Extension

The Critical Link

The Angolan section of the corridor is the most advanced in development terms, benefiting from a clearer concession framework and a more stable political environment. The DRC extension, which must connect the Angolan border at Luau through the copper belt capital of Kolwezi to the mining districts of Katanga, is the section with the greatest strategic importance and the greatest development complexity.

The DRC’s infrastructure deficit in the Katanga region is severe even by Central African standards. The primary road connecting Kolwezi to the Zambian and Angolan borders is in poor condition for significant stretches, subject to seasonal closure during the rainy season, and heavily congested with mining trucks that accelerate road degradation faster than maintenance can address it. Rail infrastructure in the Katanga region, once operated by the National Railway Company of the Congo (SNCC), has deteriorated significantly from decades of underinvestment and conflict-related damage.

The DFC financing commitment for the DRC section is specifically directed at rehabilitating and extending the rail line from the Angolan border to Kolwezi, a distance of approximately 800 kilometres. This section, once operational, eliminates the road-based intermediate leg that currently forces mining companies to truck concentrate from Katanga mines to the rail head, adding cost, transit time, and road wear that all ultimately increase the delivered cost of DRC minerals to global markets.

The DRC government under President Tshisekedi has made transport infrastructure development a stated priority, and the mining sector’s fiscal contribution to the national budget gives the government strong financial incentives to reduce logistics costs that constrain mineral export volumes and prices. The political alignment between the DRC government’s interests and the corridor’s development objectives is a positive factor, though the complexity of DRC’s institutional environment and the historical challenges of contract enforcement in the mining sector remain material considerations for project risk assessment.

The Zambian Connection

Copper Belt Integration

Zambia’s copper belt, centred on Kitwe, Ndola, and Chingola in the Copperbelt Province, produces approximately 800,000 tonnes of copper annually and hosts some of the world’s largest single copper mining operations, including Konkola Copper Mines and Lumwana. The connection of Zambia’s mining districts to the Lobito Corridor, via a rail link extending from the DRC border through Chingola to Ndola and Kitwe, is the critical step that transforms the corridor from an Angolan-DRC bilateral logistics project into a regional minerals export system.

The Zambia Railways network connects the Copperbelt to both the Tanzanian port of Dar es Salaam (via the TAZARA railway) and to the South African rail network (via the Zimbabwe and Botswana connections). Adding a high-capacity western connection through the Lobito Corridor gives Zambian copper producers genuine route competition for the first time in decades, allowing them to choose among alternative export corridors based on cost, congestion, and transit time. Port and rail competition is a proven mechanism for driving down logistics costs and improving service quality, and its introduction into the Central African minerals export system should be understood as a structural competitiveness improvement rather than merely an infrastructure addition.

The Zambian government has signed a memorandum of understanding supporting Lobito Corridor connectivity, and the African Development Bank is providing technical assistance for the feasibility study of the Zambian extension. The PGII framework includes the Zambian connection as part of the broader corridor vision, though financing for the Zambian rail section remains at an earlier stage than the Angolan and DRC components.

Beyond Minerals

The Broader Economic Corridor Logic

The investment thesis for the Lobito Corridor is typically framed around minerals logistics, and understandably so given that copper, cobalt, and lithium are the primary near-term revenue drivers. But the full economic value of the corridor extends well beyond mineral exports and develops over time as the infrastructure catalyses broader economic activity along its length.

Agricultural commodities are the most immediately significant secondary cargo category. Angola’s central highlands, through which the Benguela Railway passes, are among the most agriculturally productive zones in the country, producing maize, coffee, and horticultural products that currently have limited access to export markets due to poor road infrastructure. Rail access to Lobito port opens export routes for Angolan agricultural products that are currently viable only for domestic consumption. Similar agricultural corridor opportunities exist along the DRC and Zambian sections, where smallholder farmers and agribusiness operators currently lack cost-effective access to export markets.

Manufactured goods and consumer products moving in the opposite direction, from the port into the interior, represent the import distribution opportunity. Currently, the logistics cost of inland distribution in Central Africa is so high that it effectively restricts modern consumer goods, building materials, and industrial inputs to the largest cities and mining town economies. As the corridor reduces transport costs and transit times, the addressable market for consumer goods distribution expands progressively into secondary towns and agricultural communities along the route.

Industrial zone development along the corridor, particularly near Kolwezi in the DRC and at the Lobito port zone in Angola, is a longer-term but high-potential opportunity. Processing copper concentrate into refined copper or copper products within the DRC rather than exporting raw concentrate dramatically increases the value retained in-country. The corridor provides the logistics infrastructure that makes such processing investment viable, and both the DRC and Angolan governments have expressed clear policy intent to attract value-added processing investment to corridor-adjacent industrial zones.

Investor Entry Points

Where the Opportunities Concentrate

The Lobito Corridor creates investment opportunities across a spectrum of risk profiles and capital requirements, from the direct infrastructure of rail and port development to the adjacent logistics services and economic zone investment that the corridor enables.

For large institutional infrastructure funds, the primary opportunity is participation in the rail concession financing structure. The Lobito Atlantic Railway concession is structured to accommodate multiple tranches of debt and equity from DFI, sovereign, and commercial sources. Entry at the debt level, with DFI guarantee coverage of political and construction risk, represents a risk-adjusted return profile appropriate for pension fund and sovereign wealth fund capital seeking long-duration African infrastructure exposure.

For private equity and growth capital funds, the logistics services layer offers more accessible entry points at smaller ticket sizes. Freight forwarding, customs brokerage, warehousing, and last-mile distribution businesses positioned along the corridor will benefit from volume growth as rail capacity comes online, without requiring direct participation in the complex concession financing structures. First-mover advantage in logistics services along the corridor is real: the operators that establish route knowledge, customer relationships, and physical assets before volumes fully develop will occupy a structurally advantaged position as the corridor matures.

For specialist mining and resources investors, the corridor’s development is a direct positive catalyst for the valuation of mining assets in the Katanga region and the Zambian Copperbelt whose economics are currently penalised by high logistics costs. Projects that are marginal under current logistics cost assumptions become commercially viable when corridor-linked transport costs are applied to their financial models.

Turn Insight Into Action

We help investors, developers, and institutions move from ideas to bankable, de-risked projects across African markets.

Let’s turn your next investment into a structured success.

This article is part of Infrastructure and Trade Corridors series. The full series establishes that physical connectivity is the single largest multiplier of AfCFTA value, and that the perception of African infrastructure risk consistently overstates the actual execution record. This briefing focuses on the specific corridors, port assets, and financing instruments that are closing the gap between ambition and delivery. Read the full Infrastructure and Trade Corridors series.

Within this series:

- The Lobito port is the western terminus of the corridor and its development is directly linked to the broader port modernisation agenda across Africa. The operational efficiency improvements achieved at Tanger Med and Mombasa provide the benchmark against which Lobito’s transformation should be measured. → Read Port Modernization: Lessons from Tanger Med and Mombasa in 2026

- The Lobito Corridor’s blended finance structure, combining DFI commitments, export credit agency backing, and private concession capital, is the working model for AfCFTA infrastructure financing at scale. The financing innovations pioneered here are directly transferable to other cross-border corridor investments. → Read Financing the AfCFTA: The Role of Infrastructure Bonds and Domestic Pension Funds

Related Articles

- The DRC’s cobalt and copper are foundational materials for battery storage systems globally. The logistics cost reduction achieved by the Lobito Corridor directly improves the supply chain economics of the battery storage industry that is scaling rapidly across Africa and worldwide. → Read Battery Storage and Grid Resilience: Solving the Intermittency Gap in 2026

- The same blended finance architecture being assembled for the Lobito Corridor, combining DFI concessional capital with private concession equity and export credit agency guarantees, is the financing template being applied to large-scale green hydrogen infrastructure in Namibia. The precedents being established in corridor financing have direct application across African infrastructure asset classes. → Read The Rise of Green Hydrogen in Namibia and Morocco: Africa’s New Export Frontier

Have you Read?

De-risking African Infrastructure Investment

Public-Private Partnerships PPPs: The Future of Infrastructure in Emerging Markets

What is the AfCFTA? An Executive Overview for Global Investors

Turn Insight Into Action

We help investors, developers, and institutions move from ideas to bankable, de-risked projects across African markets.

How We Support You

- Validate opportunities with on-the-ground intelligence

- Structure investments to manage risk and attract capital

- Connect you with trusted partners, financiers, and advisors

- Navigate regulatory, financial, and operational complexity

Why It Matters

Opportunities don’t fail because they lack potential, they fail because they’re not structured to succeed.

Partner with BOH Infrastructure to unlock strategic opportunities in Africa.

Let’s turn your next investment into a structured success.

FAQ: Lobito Corridor

What is the Lobito Corridor and why is it significant for Central African development?

The Lobito Corridor is a 1,300 kilometre rail and multimodal logistics route connecting Angola’s Atlantic port of Lobito to the copper and cobalt mining districts of the DRC and Zambia. It is significant because it addresses one of the most severe logistics constraints in the global critical minerals supply chain: the extraordinary cost and difficulty of moving minerals from some of the world’s most resource-rich territories to export markets. Its development has the potential to reduce logistics costs by 30 to 50 percent for corridor-linked mining operations, transforming the economic viability of the region’s mineral sector.

Who is financing the Lobito Corridor and what is the ownership structure?

The corridor is financed through a combination of sources. The US International Development Finance Corporation has committed over USD 550 million. The European Union’s Global Gateway initiative and the African Development Bank have made additional commitments. The Angolan rail section operates under a 30-year concession awarded to the Lobito Atlantic Railway consortium comprising Trafigura, Mota-Engil, and Vecturis. DRC and Zambian sections are being financed through separate but coordinated structures currently in development.

Why is the DRC’s mineral wealth important to global clean energy supply chains?

The DRC holds approximately 70 percent of the world’s cobalt reserves, along with significant copper and emerging lithium deposits. Cobalt is a critical component of lithium-ion battery cathodes used in electric vehicles and grid-scale energy storage. Copper is essential for electrical wiring, motors, and grid infrastructure across the energy transition. The concentration of these materials in the DRC makes the country’s logistics infrastructure a strategic concern not just for African development but for the global clean energy industry.

How does the Lobito Corridor compete with China’s infrastructure investments in Central Africa?

China has been the dominant external infrastructure financier in Central Africa for two decades, typically through resource-backed loan structures exchanging infrastructure for mineral access. The Lobito Corridor offers an alternative model based on transparent concession structures, private sector financing complemented by US and EU development finance, and a logistics infrastructure focus rather than a resource extraction arrangement. The US and EU involvement is explicitly positioned as an alternative to Chinese Belt and Road engagement in the region, reflecting the geopolitical significance of critical mineral supply chain access.

What opportunities does the corridor create beyond minerals logistics?

Beyond minerals, the corridor creates agricultural export access for Angolan highland farmers and smallholder producers along the DRC and Zambian sections who currently have no cost-effective route to export markets. Import distribution economics for consumer goods, building materials, and industrial inputs improve significantly as transport costs fall. Industrial zone development adjacent to the corridor, particularly for mineral processing and value-added manufacturing, becomes viable as logistics costs decline. Over time, the corridor functions as an economic development backbone for the communities and regions along its length.

What are the main risks of investing in Lobito Corridor-linked infrastructure?

Principal risks include political and governance risk in the DRC, which has a complex institutional environment and a history of contract enforcement challenges in the mining sector. Construction and technical risk in the DRC rail extension, which involves rehabilitating severely degraded infrastructure in a logistically demanding environment. Currency and revenue risk for concession holders earning revenues in local currencies against USD-denominated financing. And geopolitical risk from the possibility that the US-China infrastructure competition dynamic that is currently accelerating the corridor’s development could shift in ways that affect financing commitments or diplomatic support.

What is the timeline for the Lobito Corridor to reach operational capacity?

The Angolan section, operated by the Lobito Atlantic Railway consortium, is the most operationally advanced component and is handling increasing freight volumes on a progressively upgraded network. The DRC extension from the Angolan border to Kolwezi, the most critical missing link, has a target completion timeline in the 2027 to 2029 range contingent on financing finalisation and construction progress. The Zambian connection is at an earlier feasibility stage, with a realistic operational timeline in the early 2030s. The trans-continental vision connecting Lobito to Dar es Salaam is a longer-term aspiration beyond a 10-year investment horizon.

Share this post:

Know someone who needs to see this? Share it with them!

Ready to explore opportunities in one of Africa’s fastest-growing markets?

Investment

Opportunities in

Africa in 2026

We provide expert guidance on market entry, due diligence, and business development support.