Battery Storage and Grid Resilience

Solving the Intermittency Gap in 2026

Every major renewable energy project built in Africa over the past decade has confronted the same fundamental constraint: the sun sets, the wind drops, and without storage or dispatchable backup generation, the lights go out. For residential consumers, intermittency is an inconvenience. For industrial operators running continuous processes, it is a deal-breaker that pushes investment decisions toward diesel generation or, more troublingly, away from African locations entirely.

The good news is that 2026 represents a genuine inflection point. Battery storage economics have crossed a threshold that makes utility-scale deployment financially viable without concessional subsidy in a growing number of African markets. The pipeline of announced BESS projects across the continent has expanded significantly, development finance institutions have begun treating storage as core infrastructure rather than a niche technology, and a new generation of grid management software is making it possible to operate complex hybrid grids with far greater reliability than was achievable even three years ago.

This article examines the structural drivers of Africa’s storage moment, the markets and business models where capital is deploying most effectively, and the risks that investors need to price carefully before committing to this still-maturing asset class.

KEY TAKEAWAYS

- Africa added more renewable generation capacity between 2022 and 2025 than in the preceding decade, but storage deployment has lagged significantly, creating a structural reliability gap that is constraining industrial investment.

- Lithium-ion battery costs have fallen over 90 percent since 2010 and crossed the USD 100 per kilowatt-hour threshold in 2024, making utility-scale BESS commercially viable across a much wider range of African project economics.

- South Africa, Kenya, and Ghana are leading continent-wide BESS deployment, driven by distinct but converging pressures: load-shedding crises, renewable integration mandates, and industrial off-taker demand.

- Decentralised mini-grid storage, pairing solar generation with battery dispatch in areas beyond the reach of national grids, represents the largest addressable storage market by number of installations and the fastest-growing by capital deployment.

- Smart grid technology, including demand response systems, digital metering, and AI-driven load forecasting, is emerging as the software layer that determines how effectively physical storage assets are utilised.

DEFINITION

Grid intermittency refers to the variable and unpredictable nature of electricity output from solar and wind generation sources. Unlike coal, gas, or geothermal plants that produce power on demand, solar panels generate only during daylight hours and wind turbines only when wind conditions are adequate.

Battery energy storage systems (BESS) are electrochemical installations that capture surplus electricity during peak generation periods and discharge it when generation falls short of demand.

Grid resilience is the broader capacity of an electricity network to maintain stable, reliable supply despite generation variability, demand spikes, infrastructure failures, or climate-related disruptions. Together, storage and resilience investment form the technical foundation that determines whether a renewable-heavy grid can reliably serve industrial consumers.

Table of Content

Battery Storage and Grid Resilience: Solving the Intermittency Gap in 2026

This article is in BOH Infrastructure’s 2026 Energy and the Green Transition series. The full series establishes that Africa’s energy deficit is overwhelmingly a financing and perception problem rather than a resource one. This briefing focuses on the specific assets, corridors, and technologies that translate that argument into investable, bankable energy infrastructure.

The Intermittency Problem in African Context

Africa’s electricity grids were not designed for high penetrations of variable renewable energy. Most national grids on the continent were built around large centralised thermal or hydropower plants that produce predictable, dispatchable output. The control systems, market structures, and grid codes that govern these networks assume a level of generation predictability that solar and wind simply do not provide without storage support.

The consequence, visible most acutely in South Africa but present in varying degrees across the continent, is that adding renewable capacity without commensurate storage investment can actually destabilise a grid rather than strengthen it. South Africa’s Eskom has on multiple occasions curtailed renewable generation from independent power producers because the grid lacked the balancing capacity to absorb output fluctuations. This curtailment destroys project returns, undermines investor confidence, and creates a perverse disincentive to build the very generation capacity the country needs.

The intermittency problem is compounded in Africa by two additional factors that are less prominent in European or North American grid contexts. First, many African grids already have high levels of hydropower, which is itself subject to seasonal variability driven by rainfall patterns. Countries like Zambia, Zimbabwe, Ethiopia, and Uganda have experienced severe power crises in recent years as droughts reduced reservoir levels, simultaneously reducing hydro output at the precise moment that demand was rising with economic growth. A grid that layers variable solar and wind on top of variable hydro without storage is compounding its vulnerability rather than diversifying it.

Second, the transmission infrastructure in most African countries is insufficient to move power efficiently from generation zones to demand centres. Even where renewable generation capacity exists, bottlenecks in the transmission network mean that storage deployed close to demand centres, rather than at generation sites, often delivers more system value. This distributed storage logic is one reason mini-grid and behind-the-meter storage models are growing faster than utility-scale centralised installations in several markets.

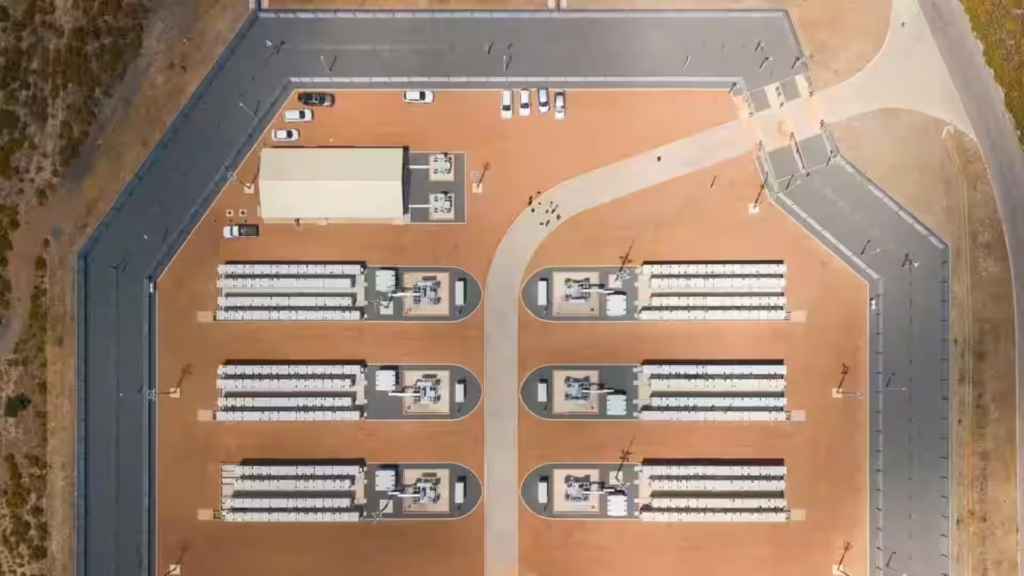

The Battery Cost Revolution and What It Means for Africa

The economics of battery storage have changed more rapidly than almost any other technology in the energy sector. Lithium-ion battery pack costs fell from approximately USD 1,200 per kilowatt-hour in 2010 to roughly USD 97 per kilowatt-hour by the end of 2024, according to BloombergNEF tracking data. This 90-plus percent cost reduction over fourteen years has fundamentally altered the business case for storage across every segment of the market.

The USD 100 per kilowatt-hour threshold is widely regarded in the industry as the point at which battery storage becomes cost-competitive with peaking gas turbines for grid balancing purposes in most market contexts. Crossing that threshold means that project developers can now include BESS in their financing models without requiring concessional support from development finance institutions to make the numbers work, at least for projects with strong off-take agreements and clear revenue visibility.

For Africa specifically, the cost reduction intersects with a second trend: the increasing availability of Chinese-manufactured lithium iron phosphate (LFP) batteries, which offer a different chemistry profile from the nickel manganese cobalt cells that dominate European and North American utility markets. LFP batteries have lower energy density but superior thermal stability, longer cycle lives (typically 4,000 to 6,000 full charge-discharge cycles versus 2,000 to 3,000 for NMC), and lower fire risk. In hot climates with limited fire suppression infrastructure, these characteristics make LFP the preferred technology for most African utility-scale deployments.

The supply chain concentration risk associated with Chinese battery manufacturing is a consideration for investors with environmental, social, and governance mandates, particularly given the cobalt and lithium sourcing questions that have attracted scrutiny in responsible investment frameworks. However, LFP batteries contain no cobalt, removing the most contentious supply chain element, and several African nations including Zimbabwe, Namibia, and the Democratic Republic of Congo are active participants in the lithium and battery minerals supply chain, creating a potential long-term domestic manufacturing pathway.

South Africa

Crisis as Catalyst

No country illustrates the urgency of storage investment more clearly than South Africa. Eskom’s load-shedding crisis, which reached stage 6 (meaning up to twelve hours of daily power cuts) for extended periods between 2022 and 2024, inflicted an estimated USD 50 billion in cumulative economic damage according to the South African Reserve Bank. It accelerated a structural shift in how South African industry approaches energy supply: away from dependence on the national grid and toward self-generation with storage backup.

The Electricity Regulation Act amendments of 2022, which removed the licensing threshold for embedded generation and allowed large consumers to sell surplus power to third parties, unleashed a wave of corporate solar and storage installations that transformed the behind-the-meter market almost overnight. By mid-2024, South Africa had installed more behind-the-meter battery storage capacity in the preceding eighteen months than in the entire preceding decade.

At the utility scale, the Bid Window 6 procurement round under the Renewable Energy Independent Power Producer Procurement Programme (REIPPPP) specifically required storage components from bidding solar and wind developers for the first time. This policy design shift signals that the South African government has accepted that renewable generation and storage must be co-procured rather than treated as separate assets. The projects awarded under Bid Window 6 represent the most significant pipeline of utility-scale storage construction in Sub-Saharan Africa currently in development.

For investors, South Africa’s storage market offers a rare combination of scale, institutional capacity, and clear policy signals. The risks, primarily Eskom’s financial fragility and the complexity of navigating the REIPPPP procurement process, are well understood and already priced into the market. The more interesting opportunity may be in the C and I (commercial and industrial) segment, where the combination of high diesel costs, improving battery economics, and new regulations permitting wheeling of power across the grid is creating a rapidly expanding addressable market for specialist energy service companies.

Kenya and East Africa

Storage as the Missing Link

Kenya’s grid presents a different but equally instructive storage challenge. Unlike South Africa, Kenya does not have a coal problem. Its grid is already over 90 percent renewable by installed capacity, drawing on geothermal, hydro, wind (the Lake Turkana Wind Power project is the largest wind farm in Africa), and growing solar. The intermittency challenge in Kenya is therefore not about transitioning away from fossil fuels but about managing the interaction between multiple variable generation sources and a demand profile that is growing faster than transmission infrastructure can keep pace with.

The Lake Turkana wind farm, while transformational in scale at 310 MW, highlighted the transmission bottleneck problem sharply. For several years after commissioning, a significant portion of its potential output was curtailed because the transmission line connecting the remote northern Kenya site to the national grid was not completed on schedule. Storage co-located at generation sites can partially mitigate this curtailment problem by smoothing output profiles and reducing the peak transmission capacity required, a design principle now being incorporated into new Kenyan renewable projects.

Kenya’s Vision 2030 energy planning framework and the broader East African Power Pool interconnection agenda create strong long-term demand signals for grid-scale storage, particularly at key nodes in the regional transmission network where cross-border power flows require balancing capacity. The East African Development Bank and the African Development Bank have both indicated storage as a priority financing area for the 2026 to 2030 planning cycle.

The Mini-Grid Storage Opportunity

Beyond utility-scale and behind-the-meter installations, the mini-grid segment represents what is arguably Africa’s most distinctive and fastest-growing storage market. An estimated 600 million Africans remain without reliable electricity access, the vast majority in rural and peri-urban communities that are too dispersed or too distant from existing grid infrastructure to be connected within any credible national electrification timeline.

Solar-plus-storage mini-grids, where a localised solar generation system paired with battery storage serves a defined community or economic zone, have emerged as the technically and economically proven solution for this market. The business model has matured considerably over the past five years. Anchor commercial customers, typically telecoms towers, agro-processing facilities, schools, or health clinics, provide the base load revenue that makes the mini-grid financially viable, with residential and small commercial consumers served on a tiered tariff structure.

Companies operating in this space, including CrossBoundary Energy Access, Husk Power Systems, and Sun King (formerly Greenlight Planet), have demonstrated that mini-grid portfolios can generate risk-adjusted returns comparable to conventional infrastructure assets when structured correctly. The key variables are anchor customer mix, battery cycle life management, and the ability to refinance construction debt with lower-cost capital once operational track records are established.

Development finance institutions including the IFC, FMO, and the British International Investment have all increased allocation to mini-grid platforms in the 2024 to 2026 period, in part because the aggregation of multiple mini-grid sites into a single investment vehicle addresses the ticket size problem that previously made individual projects too small for institutional capital.

Turn Insight Into Action

We help investors, developers, and institutions move from ideas to bankable, de-risked projects across African markets.

Let’s turn your next investment into a structured success.

Smart Grid Technology

The Software Layer

Physical storage assets are only as valuable as the software systems managing their dispatch. A battery that charges and discharges on a naive schedule, without forecasting demand, predicting generation variability, or optimising against time-of-use tariff structures, delivers a fraction of the value of an equivalent battery managed by an intelligent energy management system.

The smart grid technology market in Africa is growing rapidly, driven by the combination of falling sensor and metering costs, increasing mobile and data connectivity across the continent, and the growing complexity of grids that must balance multiple generation sources, storage assets, and increasingly active demand-side participants. AI-driven load forecasting, which uses weather data, historical consumption patterns, and real-time sensor feeds to predict demand and generation with sufficient accuracy to optimise storage dispatch, is now commercially available from several providers at price points accessible to mid-scale African utilities.

Advanced metering infrastructure, which replaces traditional electromechanical meters with digital meters capable of two-way communication and time-of-use measurement, is the foundational data layer for demand response programmes. Several African utilities, including Kenya Power and the Electricity Company of Ghana, have active advanced metering rollout programmes that will progressively enable more sophisticated grid management as penetration increases.

For investors, the smart grid software and services market is a high-growth, capital-light opportunity that sits adjacent to the heavier infrastructure plays in generation and storage. Companies with proven platforms and the ability to localise for African grid architectures and regulatory environments are well positioned as utility digitalisation accelerates.

Risk Register for Battery Storage Investment in Africa

Storage investment in Africa carries four principal risks that require careful modelling. First, technology evolution risk: battery chemistry and management system technology are still advancing rapidly, and assets commissioned today may face obsolescence pressure from superior technologies within their projected economic lives. Second, revenue certainty risk: in markets without well-developed capacity payment mechanisms or time-of-use tariff structures, the revenue model for storage assets can be difficult to underwrite with the certainty that project finance lenders require. Third, grid code and regulatory risk: many African jurisdictions have grid codes that were not designed for storage assets and may create operational constraints or dispatch conflicts that reduce asset utilisation. Fourth, foreign exchange risk: battery equipment is predominantly priced in USD or euros, while storage revenue is typically earned in local currencies, creating a structural mismatch that must be hedged or absorbed in project economics.

This article is part of Energy and the Green Transition series. The full series establishes that Africa’s energy deficit is overwhelmingly a financing and perception problem rather than a resource one. This briefing focuses on the specific assets, corridors, and technologies that translate that argument into investable, bankable energy infrastructure. Read the full Energy and the Green Transition series.

Within this series:

- Kenya’s low-cost geothermal electricity positions it as a future green hydrogen producer alongside North and Southern African pioneers. → Read The Rise of Green Hydrogen in Namibia and Morocco: Africa’s New Export Frontier

- Kenya’s low-cost geothermal electricity positions it as a complementary green hydrogen producer to Namibia and Morocco, with a different feedstock profile and a primarily domestic industrialisation focus in the near term. → Read Kenya’s Geothermal Advantage: A Blueprint for Regional Energy Security

Related Articles

- Data centres are among the most demanding commercial and industrial consumers of reliable electricity. Storage investment enabling grid reliability is a direct prerequisite for the data centre development agenda across Nigeria and East Africa. → Read The Infrastructure of AI: Nigeria’s First Dedicated Data Centres

- The blended finance instruments being developed for cross-border infrastructure have direct applications to regional storage and grid interconnection projects, where the benefits are multi-jurisdictional but the financing must be structured nationally. → Read Financing the AfCFTA: The Role of Infrastructure Bonds and Domestic Pension Funds

Have you Read?

De-risking African Infrastructure Investment

Public-Private Partnerships PPPs: The Future of Infrastructure in Emerging Markets

What is the AfCFTA? An Executive Overview for Global Investors

Turn Insight Into Action

We help investors, developers, and institutions move from ideas to bankable, de-risked projects across African markets.

How We Support You

- Validate opportunities with on-the-ground intelligence

- Structure investments to manage risk and attract capital

- Connect you with trusted partners, financiers, and advisors

- Navigate regulatory, financial, and operational complexity

Why It Matters

Opportunities don’t fail because they lack potential, they fail because they’re not structured to succeed.

Partner with BOH Infrastructure to unlock strategic opportunities in Africa.

Let’s turn your next investment into a structured success.

FAQ: Battery Storage and Grid Resilience

Why is battery storage important for Africa’s electricity grids in 2026?

Most African grids have added significant solar and wind capacity over the past decade, but storage deployment has lagged behind. Without storage, variable renewable generation creates frequency and voltage instability that constrains how much renewable capacity a grid can absorb. Storage provides the balancing function that allows renewable penetration to increase without compromising reliability for industrial and residential consumers.

What type of battery technology is most commonly used for utility-scale storage in Africa?

Lithium iron phosphate (LFP) batteries dominate new utility-scale deployments in Africa. Compared to other lithium-ion chemistries, LFP offers superior thermal stability, longer cycle life (4,000 to 6,000 cycles), lower fire risk, and no cobalt content. These characteristics make LFP well suited to hot climates and locations with limited maintenance infrastructure.

How has the cost of battery storage changed and what does it mean for African projects?

Lithium-ion battery pack costs have fallen over 90 percent since 2010, crossing the USD 100 per kilowatt-hour threshold in 2024. This cost level makes utility-scale battery storage commercially viable without concessional subsidy in markets with clear revenue mechanisms, substantially broadening the universe of viable projects across the continent.

What is a solar-plus-storage mini-grid and why is it relevant for rural Africa?

A solar-plus-storage mini-grid is a localised electricity system combining solar panels with battery storage to serve a defined community or economic zone that is not connected to the national grid. It is the most cost-effective and technically proven solution for rural electrification in Africa, where grid extension to dispersed communities is prohibitively expensive. Anchor commercial customers such as telecoms towers, health clinics, and agro-processors provide the revenue base that makes mini-grid businesses financially viable.

What is smart grid technology and how does it improve storage performance?

Smart grid technology encompasses digital metering, real-time sensor networks, demand response systems, and AI-driven load forecasting. Together, these tools allow grid operators and storage asset managers to optimise when batteries charge and discharge, predict generation and demand variability, and coordinate multiple assets across a network. An intelligently managed battery delivers significantly more grid value than the same physical battery operating on a fixed schedule.

What are the main risks of investing in battery storage assets in Africa?

The four principal risks are: technology evolution risk as battery chemistry continues to advance; revenue certainty risk in markets without mature capacity payment or time-of-use tariff structures; grid code and regulatory risk in jurisdictions whose rules were not designed for storage; and foreign exchange risk from the mismatch between USD-priced equipment and local-currency revenues.

Which African countries are leading battery storage deployment in 2026?

South Africa leads by installed capacity, driven by the load-shedding crisis that forced large-scale corporate and utility adoption. Kenya is the most advanced in East Africa, supported by its mature renewable energy policy framework and the Lake Turkana wind integration challenge. Ghana is emerging as a West African leader, with several utility-scale BESS projects in the procurement pipeline. Nigeria has significant potential but regulatory uncertainty has slowed deployment relative to its market size.

Share this post:

Know someone who needs to see this? Share it with them!

Ready to explore opportunities in one of Africa’s fastest-growing markets?

Investment

Opportunities in

Africa in 2026

We provide expert guidance on market entry, due diligence, and business development support.