What is the AfCFTA? An Executive Overview for Global Investors

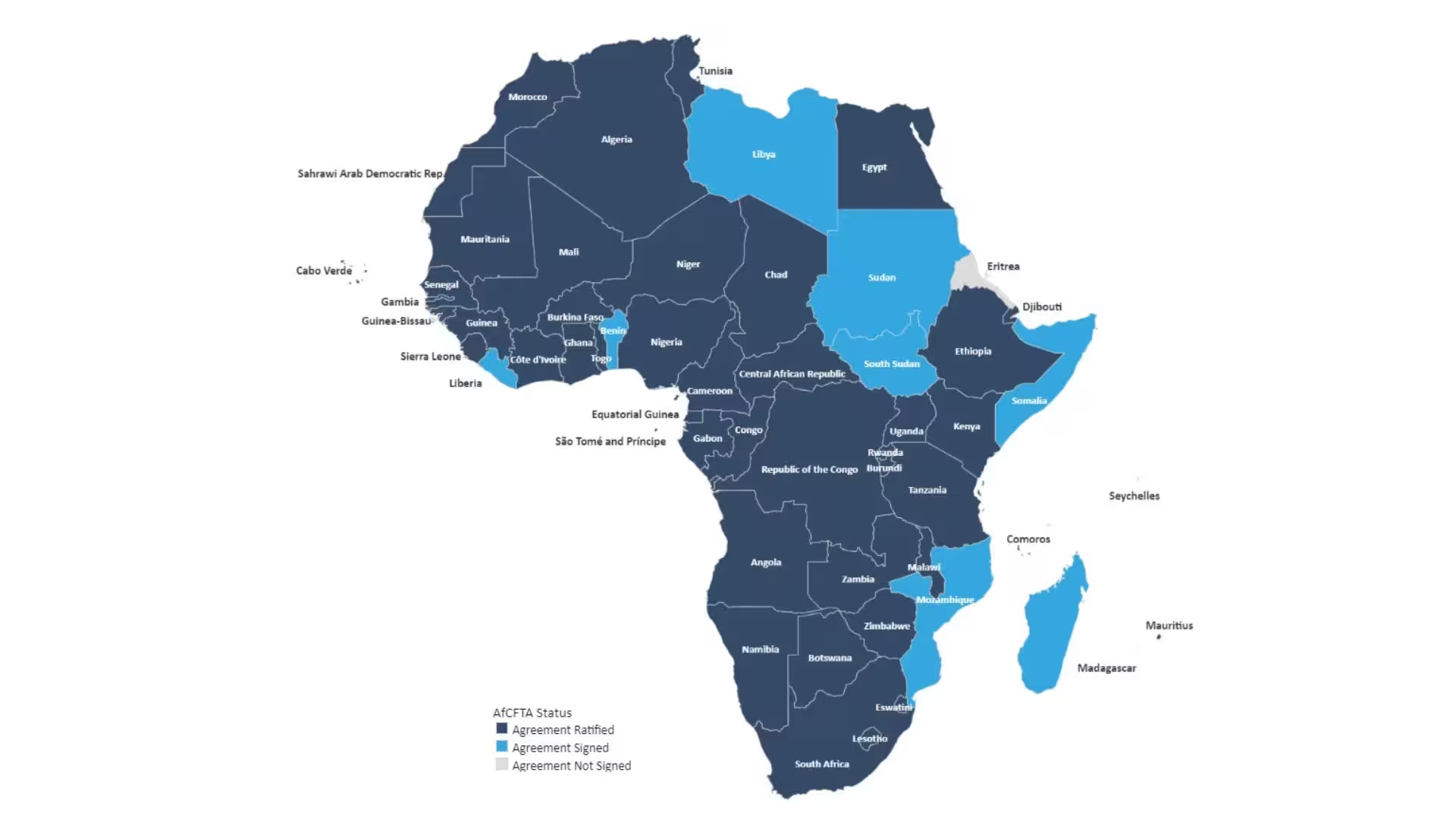

Membership of the AfCFTA

The membership of the AfCFTA comprises 54 out of 55 African states recognised by the African Union.

Source: Africa Trade Foundation

Africa accounts for approximately 17 percent of the world’s population and holds an estimated 30 percent of the world’s mineral reserves, 60 percent of its uncultivated arable land, and the fastest-growing working-age population of any region on earth. Yet the continent’s 55 nations collectively generate only 3 percent of global GDP and conduct less than 3 percent of global trade. The gap between Africa’s resource endowment and its economic output is the defining development challenge of the twenty-first century, and the AfCFTA is the most ambitious and comprehensive attempt ever made to close it.

The agreement is not, at its core, a tariff reduction exercise. Tariffs on intra-African trade are already relatively low in most corridors, averaging around 6 percent compared to over 10 percent for goods entering Africa from outside the continent. The AfCFTA’s deeper significance is structural: it creates the legal, regulatory, and institutional architecture for a continental market that can attract the manufacturing investment, supply chain development, and financial services integration that have driven economic transformation in East Asia, Southeast Asia, and more recently South Asia.

For institutional investors, the AfCFTA is best understood not as a policy achievement to be celebrated but as a market creating event to be positioned for. The agreement is in the early stages of implementation. The infrastructure being built to support it is at various stages of financing and construction. The regulatory harmonisation it requires is being negotiated sector by sector across dozens of national jurisdictions. The investors who build analytical frameworks and market relationships during this implementation phase will be positioned to deploy capital into a continental market that will look structurally different in a decade from the fragmented one they observe today.

KEY TAKEAWAYS

- The AfCFTA creates the world’s largest free trade area by participating nations, covering 55 economies, 1.4 billion people, and a combined GDP of approximately USD 3.4 trillion, with the potential to add a further USD 450 billion to African income levels by 2035 under full implementation scenarios.

- Intra-African trade currently represents only 15 to 18 percent of Africa’s total trade, compared to 60 to 70 percent for Europe and over 50 percent for Asia, indicating that the structural integration opportunity is at a very early stage relative to its long-term potential.

- The agreement eliminates tariffs on 90 percent of goods over phased timelines of 5, 10, or 13 years depending on a member state’s classification, with the most sensitive 7 percent of tariff lines subject to special treatment and 3 percent fully excluded.

- The Pan-African Payment and Settlement System (PAPSS), launched alongside the AfCFTA framework, enables cross-border transactions in African local currencies, addressing one of the most significant practical barriers to intra-African commercial activity: the USD dependency of regional trade finance.

- The AfCFTA’s success depends critically on resolving an estimated USD 130 to USD 170 billion annual infrastructure financing gap, covering transport corridors, energy interconnection, and digital connectivity, without which tariff elimination on paper cannot translate into commercially viable trade flows in practice.

DEFINITION

The African Continental Free Trade Area (AfCFTA) is a continental trade agreement, formally established by the AfCFTA Agreement signed in Kigali, Rwanda in March 2018 and operational since January 1, 2021, that creates a single market for goods and services across all 55 member states of the African Union. It is a flagship project of the African Union’s Agenda 2063 long-term development framework and is recognised by the World Trade Organization as the largest free trade area in the world by number of participating countries. The agreement commits member states to the phased elimination of tariffs on the majority of intra-African trade, the progressive harmonisation of trade rules, standards, and customs procedures, and the liberalisation of trade in services including finance, transport, telecommunications, and professional services. Its ultimate objective is the transformation of Africa from a collection of 55 largely disconnected national economies into a single integrated continental market capable of driving industrial development, attracting global investment, and delivering sustained economic growth for its 1.4 billion citizens.

Table of Content

Origins and Governance Architecture

The AfCFTA was not conceived overnight. Its intellectual foundations lie in the Lagos Plan of Action of 1980, which first articulated the vision of African economic integration, and in the Abuja Treaty of 1991, which established the African Economic Community and defined a six-stage roadmap toward continental economic integration over a 34-year timeline. The AfCFTA accelerated this timeline significantly: what the Abuja Treaty projected would take three decades was compressed into a framework agreement negotiated and ratified within five years.

The agreement was endorsed by 44 of 55 African Union member states at the Extraordinary AU Summit in Kigali in March 2018, a show of political consensus that was genuinely significant given the historical difficulty of achieving continental-scale agreement on trade policy. The AfCFTA entered into force in May 2019 after the threshold of 22 ratifications was reached, and trading under its preferential tariff framework began on January 1, 2021.

The AfCFTA Secretariat, based in Accra, Ghana, serves as the treaty body responsible for coordinating implementation, supporting negotiations on outstanding protocols, and monitoring member state compliance. The Secretariat operates under the authority of the African Union but functions as an independent institution with a dedicated staff and budget. Its effectiveness is constrained by resource limitations relative to the scale of its mandate, but its institutional presence provides the coordination architecture that bilateral and multilateral infrastructure financing decisions require.

The governance structure also includes a Committee of Senior Trade Officials responsible for technical negotiation, a Council of Ministers of Trade that provides political direction, and an Assembly-level Summit that reviews implementation progress. Dispute resolution is handled through a dedicated AfCFTA dispute settlement mechanism modelled broadly on WTO practice, providing a formal institutional channel for resolving trade conflicts that previously had no continent-wide resolution framework.

The Tariff Reduction Architecture

The AfCFTA’s tariff elimination framework is more nuanced than the headline “97 percent tariff elimination” figure suggests, and understanding its structure is important for investors assessing specific trade flow and logistics investment opportunities.

Member states are classified into three groups for tariff reduction purposes. Developing country members, which comprise the majority of AU member states, commit to eliminating tariffs on 90 percent of tariff lines over a five-year period from the date of their scheduled commencement. Least Developed Country (LDC) members have a 10-year timeline for the same 90 percent reduction. A further 7 percent of tariff lines are designated “sensitive products,” subject to longer phase-in periods of up to 13 years. The remaining 3 percent are excluded products, typically covering items considered strategically sensitive on food security, industrial policy, or revenue protection grounds.

The non-tariff barriers (NTBs) that the AfCFTA also addresses are, in many corridors, more commercially significant than the tariffs themselves. NTBs include duplicative border documentation requirements, inconsistent standards and conformity assessment procedures, discriminatory licensing and regulatory approvals, and the informal payments that accumulate at poorly governed border crossings. The AfCFTA’s NTB elimination programme requires member states to notify existing NTBs, commit to their elimination within defined timelines, and report progress through a dedicated monitoring mechanism. This process is slower and less linear than tariff reduction but is arguably more economically significant for sectors such as agriculture, manufacturing, and logistics services.

Rules of Origin, which define how much local content a product must contain to qualify for preferential tariff treatment under the agreement, are a critical technical dimension of AfCFTA implementation that directly affects investment location decisions. A manufacturer choosing between production locations in different African countries needs to know whether the product it intends to make will qualify as “African origin” for AfCFTA purposes. The Rules of Origin negotiations, which have been among the most technically complex aspects of AfCFTA implementation, were substantially completed by 2024 and are being progressively refined by sector.

The Scale of the Market Opportunity

The economic projections for full AfCFTA implementation are genuinely transformative, though they require careful contextualisation because they assume sustained political commitment to implementation over a decade or more, along with the infrastructure investment and institutional reform that the agreement’s trade liberalisation provisions cannot themselves deliver.

The World Bank’s most widely cited AfCFTA impact assessment projects that full implementation could increase intra-African exports by 81 percent, raise total African exports by 29 percent, and lift 68 million people out of moderate poverty by 2035. The income gains are estimated at USD 450 billion, with the largest benefits accruing to countries with the most diversified manufacturing bases and the best-developed transport connectivity to regional markets.

The United Nations Economic Commission for Africa (UNECA) estimates that intra-African trade could increase from its current 15 to 18 percent share of total African trade to 52 percent under full implementation, a shift that would represent one of the most significant reorientations of trade geography of any world region in the post-war era.

These projections are conditional on infrastructure development. The most economically integrated regions of the world, Europe, East Asia, and North America, all achieved their integration levels on the back of extensive transport, energy, and digital connectivity infrastructure built over decades. Africa’s integration trajectory will be determined by whether equivalent infrastructure investment occurs. The infrastructure financing gap of USD 130 to USD 170 billion annually is therefore not a separate economic development issue from the AfCFTA. It is the AfCFTA’s central implementation challenge.

From Extraction to Value Chains

The AfCFTA’s most consequential long-term impact on African economic structure is not the trade it facilitates between existing industries but the industrial development it enables by creating a sufficiently large domestic market to justify the scale of manufacturing investment that generates genuine value-added production.

The “small market problem” has historically been one of the most binding constraints on African industrialisation. A manufacturing investor considering whether to build a plant capable of producing at competitive scale faces a fundamental question: is the addressable market large enough to support the output of a minimum efficient scale facility? In most individual African countries, the answer for most categories of manufactured goods is no. A competitive cement plant, a minimum-scale pharmaceutical manufacturer, a viable automobile assembly operation, or a competitive electronics assembly facility all require markets larger than most individual African economies can support.

The AfCFTA changes this calculus by replacing 55 national markets with a single continental one. A pharmaceutical manufacturer can now design a production facility for a market of 1.4 billion people, exporting across the continent under unified quality standards and preferential tariff treatment. A textile and apparel manufacturer can invest in the most cost-competitive African production location and serve the entire continental consumer market without the tariff barriers that previously forced regional manufacturers to replicate small-scale facilities in each national market rather than achieving economies of scale in a single location.

The regional value chain development that this creates is the AfCFTA’s most significant long-term contribution to the structural transformation of African economies. Africa’s critical minerals (cobalt, copper, lithium, manganese, and platinum group metals) can be processed within Africa using African energy and African labour, producing battery components, refined metals, and chemical inputs for continental manufacturing rather than raw materials for export. West African cocoa can be processed into chocolate for an African consumer market of hundreds of millions rather than exported as beans for European processing. East African cut flowers, horticultural products, and coffee can be processed and packaged to African quality standards for intra-African premium consumption as well as export.

This shift from raw material export toward value chain integration is not just an economic development objective. It is a commercial investment thesis. The companies and investors that build processing, manufacturing, and distribution infrastructure aligned with AfCFTA value chain development will capture the margin currently accruing to processors and brand owners in consuming country markets.

The Pan-African Payment and Settlement System (PAPSS)

One of the most practically significant innovations embedded in the AfCFTA framework is the Pan-African Payment and Settlement System, developed by Afreximbank in collaboration with the AfCFTA Secretariat and launched commercially in 2022.

PAPSS addresses a specific and commercially important friction in intra-African trade that is invisible to external observers but acutely felt by African businesses: the difficulty of settling cross-border transactions in African local currencies. Currently, a Kenyan company buying goods from a Nigerian supplier must typically convert Kenyan shillings to US dollars, transfer the dollars internationally, and then the Nigerian supplier must convert dollars to naira. This process involves two currency conversion fees, international wire transfer charges, correspondent banking fees, and exposure to exchange rate movements during the settlement window. For small and medium-sized enterprises, these friction costs can represent 3 to 8 percent of transaction value, creating an effective tariff on intra-African trade that no trade agreement can eliminate because it is embedded in banking infrastructure rather than customs policy.

PAPSS allows the same transaction to be settled directly between Kenyan shillings and Nigerian naira, with Afreximbank providing the central clearing and net settlement function. The cost reduction is significant, particularly for SME traders operating in multiple African markets, and the elimination of USD dependency reduces the exposure of intra-African trade to US monetary policy and correspondent banking decisions by US financial institutions.

For investors in African financial services, PAPSS represents both a competitive threat to existing correspondent banking arrangements and a commercial infrastructure investment in its own right. The network of African central banks and commercial banks participating in PAPSS is growing, and the transaction volumes being processed through the system are increasing as awareness and technical integration expand.

Sector-Specific Investment Implications

The AfCFTA creates differentiated investment implications across sectors, and institutional investors need to think through these sector-specific dynamics rather than treating AfCFTA as a generic Africa investment thesis.

🔵 Manufacturing and industrial processing is the sector with the largest structural benefit from AfCFTA market integration. The combination of enlarged addressable market, Rules of Origin incentives that reward local content, and progressive harmonisation of product standards creates a compelling case for greenfield manufacturing investment in strategically located African countries with good infrastructure connectivity, competitive energy costs, and access to regional distribution networks.

🔵 Financial services face both opportunity and disruption. The AfCFTA’s financial services liberalisation protocol will progressively open African banking, insurance, and capital markets to cross-border competition, creating expansion opportunities for well-capitalised pan-African financial institutions and challenging incumbents whose profitability depends on protected national market positions. The development of cross-border payment infrastructure through PAPSS creates a new category of financial infrastructure investment opportunity.

🔵 Logistics and transport is the sector most directly and immediately affected by AfCFTA implementation. Every unit of incremental intra-African trade requires a logistics transaction. The development of regional transport corridors, border crossing modernisation, customs digitalisation, and multimodal freight infrastructure is both a prerequisite for AfCFTA trade growth and a direct commercial opportunity for logistics investors.

🔵 Agriculture and food processing benefits from the AfCFTA’s creation of a continental food market in which African countries can specialise in producing the crops best suited to their climate and soil conditions, trading with neighbouring countries that produce complementary agricultural products. The elimination of intra-African agricultural tariffs and the harmonisation of sanitary and phytosanitary standards reduces the cost of cross-border agricultural trade and enables the development of regional food value chains that are more resilient, more efficient, and more economically beneficial than the current pattern of agricultural self-sufficiency within fragmented national markets.

🔵 Digital economy and technology is the sector where AfCFTA’s services trade liberalisation and digital trade protocol are creating the conditions for genuinely continental-scale digital businesses. A fintech, e-commerce, or digital services company that previously had to navigate 55 separate regulatory environments to serve the African market has a significantly clearer path to continental scale under a harmonised AfCFTA digital trade framework.

Implementation Challenges and Risk Factors

An honest assessment of the AfCFTA must engage with the implementation challenges that sit between the agreement’s ambitions and their realisation.

The implementation record to date is mixed. The Guided Trade Initiative, launched in 2022 to begin operationalising AfCFTA trade in a pilot cohort of member states, has demonstrated that AfCFTA-preferential trade transactions are technically feasible but has also revealed significant bottlenecks in customs procedures, rules of origin documentation, and trader awareness that require sustained technical assistance and institutional capacity building to resolve.

Several member states have been slow to submit their tariff offers and commit to implementation schedules, reflecting the domestic political economy of trade liberalisation: industries that benefit from current tariff protection are well organised in opposing liberalisation, while the diffuse consumer and economy-wide benefits of integration are harder to mobilise politically. The AfCFTA Secretariat’s enforcement mechanisms are limited relative to those available to the WTO, and the prospect of formal dispute resolution between African member states over AfCFTA commitments remains largely theoretical.

Infrastructure remains the most binding implementation constraint. The AfCFTA Secretariat can negotiate preferential tariffs and harmonise regulations, but it cannot build roads, railways, or power grids. The infrastructure investment required to make AfCFTA trade flows physically viable at scale requires financing decisions and implementation capacity that lie entirely outside the agreement’s institutional remit.

Currency volatility and macroeconomic instability in several member states create transactional uncertainty for intra-African traders that PAPSS partially addresses but cannot fully resolve. An exporter pricing goods in naira for a Kenyan buyer is exposed to naira volatility in a way that an exporter pricing in dollars is not, and PAPSS’s net settlement model reduces but does not eliminate this exposure.

The Investor’s Strategic Framework

For institutional investors approaching the AfCFTA as a market thesis rather than a policy topic, the strategic framework involves three analytical dimensions.

The first is identifying which sectors and geographies are positioned to benefit most from AfCFTA integration within a 5 to 10 year investment horizon, focusing on the initial implementation phase rather than the full long-term potential. Manufacturing hub countries with good infrastructure, competitive energy, and strong rule of law (including Morocco, Kenya, Ethiopia, South Africa, and Rwanda) are the early beneficiaries. Logistics corridor investments, particularly those linking these hub economies to regional markets, offer the most immediate revenue visibility.

The second is assessing which specific investment instruments provide the most appropriate risk-return exposure to the AfCFTA thesis. Direct equity in AfCFTA-aligned manufacturing or logistics businesses provides the highest potential upside but requires operational engagement and local market knowledge. Infrastructure debt and infrastructure bond instruments provide lower but more predictable returns with longer duration. Development finance co-investment structures provide blended risk-return profiles that allow institutional investors to access African infrastructure with partial risk mitigation from DFI guarantee coverage.

The third is monitoring implementation progress as the primary leading indicator of when specific investment deployments are most timely. The AfCFTA’s economic value creation is not linear: it will accelerate as critical infrastructure milestones are reached, as PAPSS adoption expands, and as Rules of Origin frameworks are fully operationalised across key manufacturing sectors. Investors who build the analytical infrastructure to monitor these implementation signals will be best positioned to deploy capital at the inflection points where AfCFTA-driven value creation accelerates.

Turn Insight Into Action

We help investors, developers, and institutions move from ideas to bankable, de-risked projects across African markets.

Let’s turn your next investment into a structured success.

Related Articles

These articles examine specific dimensions of the infrastructure, industrial, and financing conditions that determine whether AfCFTA’s transformative potential is realised.

Energy and the Green Transition

- Affordable, reliable energy is a prerequisite for AfCFTA manufacturing competitiveness. Kenya’s geothermal advantage positions it as an energy-secure manufacturing hub for East African regional value chains. → Read Kenya’s Geothermal Advantage: A Blueprint for Regional Energy Security

- Regional energy interconnection, essential for AfCFTA energy integration across the East African Power Pool and Southern African Power Pool, depends on the grid resilience investments examined in this article. → Read Battery Storage and Grid Resilience: Solving the Intermittency Gap in 2026

Agribusiness and Food Security

- The AfCFTA creates the continental market scale that justifies investment in West African chocolate manufacturing, enabling local value chain capture that the fragmented pre-AfCFTA market could not support. → Read From Cocoa to Chocolate: The Industrialization of West African Agribusiness

- Intra-African agricultural trade, one of the largest near-term AfCFTA trade flow categories, depends on cold chain infrastructure development to make perishable commodity trade commercially viable at scale. → Read Cold Chain Logistics: The USD 50 Billion Opportunity in Africa’s Perishable Markets

Digital Economy and Fintech 2.0

- PAPSS and AfCFTA financial services liberalisation are accelerating the consolidation of African fintech platforms into pan-continental financial ecosystems. → Read Fintech Consolidation 2026: Why Super-Apps are Dominating Tier-1 Markets

- The AfCFTA’s progressive harmonisation of financial services regulation is the macro framework within which African fintech’s regulatory compliance advantage is being built. → Read Regulatory Compliance as a Competitive Advantage in African Fintech

Infrastructure and Trade Corridors

- The Lobito Corridor is the most advanced practical expression of the AfCFTA’s transport infrastructure agenda in Central Africa. → Read The Lobito Corridor: Reimagining Central African Logistics

- Port efficiency is the maritime gateway condition for AfCFTA trade competitiveness. Port modernisation investment is the most commercially immediate AfCFTA infrastructure opportunity. → Read Port Modernization: Lessons from Tanger Med and Mombasa in 2026

- The financing architecture for AfCFTA infrastructure, combining domestic pension capital, DFI credit enhancement, and infrastructure bond instruments, is examined in full detail in this companion article. → Read Financing the AfCFTA: The Role of Infrastructure Bonds and Domestic Pension Funds

Have you Read?

De-risking African Infrastructure Investment

Public-Private Partnerships PPPs: The Future of Infrastructure in Emerging Markets

Turn Insight Into Action

We help investors, developers, and institutions move from ideas to bankable, de-risked projects across African markets.

How We Support You

- Validate opportunities with on-the-ground intelligence

- Structure investments to manage risk and attract capital

- Connect you with trusted partners, financiers, and advisors

- Navigate regulatory, financial, and operational complexity

Why It Matters

Opportunities don’t fail because they lack potential, they fail because they’re not structured to succeed.

Partner with BOH Infrastructure to unlock strategic opportunities in Africa.

Let’s turn your next investment into a structured success.

FAQ: The AfCFTA

What is the AfCFTA and when did it come into effect?

The African Continental Free Trade Area is a continental trade agreement creating a single market across all 55 African Union member states. The agreement was signed in Kigali, Rwanda in March 2018, entered into legal force in May 2019 after reaching the required 22 ratifications, and began operating as a preferential trade framework on January 1, 2021. It is the world’s largest free trade area by number of participating countries.

How large is the AfCFTA market and what is its economic potential?

The AfCFTA covers a combined GDP of approximately USD 3.4 trillion and a population of 1.4 billion people. Under full implementation, the World Bank projects it could increase intra-African exports by 81 percent, lift 68 million people out of moderate poverty, and add USD 450 billion to African income levels by 2035. The UNECA projects that intra-African trade could grow from its current 15 to 18 percent of total African trade to over 50 percent under full integration.

How does the AfCFTA’s tariff elimination work?

The agreement eliminates tariffs on 90 percent of goods traded between African countries over phased timelines: five years for developing country members, and ten years for Least Developed Country members. A further seven percent of tariff lines covering sensitive products have longer phase-in periods of up to thirteen years. Three percent of tariff lines are excluded entirely, typically for food security, industrial policy, or revenue protection reasons.

What is the Pan-African Payment and Settlement System (PAPSS)?

PAPSS is a cross-border payment infrastructure, developed by Afreximbank and launched commercially in 2022, that enables intra-African trade transactions to be settled directly in African local currencies rather than requiring conversion through US dollars. It reduces the transaction cost of intra-African trade for businesses, eliminates the USD dependency that exposes regional trade to US monetary policy, and provides a practical mechanism for implementing the AfCFTA’s financial services integration objectives.

Why is infrastructure investment so critical to AfCFTA success?

The AfCFTA removes legal and regulatory barriers to intra-African trade, but it cannot remove physical barriers. Countries cannot trade efficiently if the roads connecting their markets are impassable, if railway networks stop at national borders, or if energy grids cannot supply the reliable electricity manufacturing requires. The African Development Bank estimates an annual infrastructure financing gap of USD 130 to USD 170 billion for the transport, energy, and digital infrastructure required to make AfCFTA trade flows commercially viable at scale. Resolving this gap is the most important implementation challenge the agreement faces.

What are the main risks to AfCFTA implementation?

The principal risks are: uneven and slow member state implementation of tariff reduction commitments and NTB elimination; the infrastructure financing gap remaining unresolved at the required scale and pace; currency volatility and macroeconomic instability creating transactional uncertainty for intra-African traders; political economy resistance from protected domestic industries opposing liberalisation; and the limited enforcement capacity of the AfCFTA Secretariat relative to the scale of its implementation mandate.

Which African countries are best positioned to benefit from AfCFTA in the near term?

Countries with established manufacturing capacity, good transport connectivity, competitive and reliable energy infrastructure, and strong institutional environments are best positioned for near-term AfCFTA benefit. Morocco (for North and West African manufacturing and logistics), Kenya and Ethiopia (for East African manufacturing and services), South Africa (for Southern African manufacturing and financial services), Rwanda (for services and digital economy), and Nigeria (for West African consumer market access given its population scale) are most frequently cited by economic analysis as early AfCFTA beneficiaries. The common characteristic across these countries is infrastructure quality sufficient to make AfCFTA trade flows operationally viable before the full infrastructure investment programme is complete.

How does the AfCFTA relate to existing regional trade agreements like ECOWAS and the EAC?

The AfCFTA sits above existing regional economic communities (RECs) including ECOWAS, the East African Community, SADC, COMESA, and others in the African trade architecture. It does not replace these agreements but extends their preferential trading arrangements to the continental level, creating preferences between regions that previously traded on most-favoured nation terms. Member states can maintain their existing REC commitments while implementing AfCFTA obligations, though where REC and AfCFTA provisions overlap, the more liberalising commitment generally prevails. Over time, the AfCFTA is expected to provide the architecture for rationalising the overlapping membership of multiple RECs that currently creates the “spaghetti bowl” complexity of African regional trade arrangements.

What role does the African Development Bank play in AfCFTA implementation?

The African Development Bank is the AfCFTA’s primary multilateral development finance partner, providing three distinct contributions: infrastructure financing for priority trade corridors and energy interconnection projects identified in the Programme for Infrastructure Development in Africa (PIDA); technical assistance to member states for customs modernisation, trade facilitation reform, and AfCFTA implementation capacity; and financial intermediation through the Africa50 infrastructure fund, which mobilises African institutional capital for AfCFTA-aligned infrastructure investment. The AfDB’s annual lending capacity of approximately USD 10 billion is insufficient to close the infrastructure financing gap independently, but its catalytic role in blended finance structures is essential to mobilising the private and institutional capital that must fill the majority of the gap.

How should institutional investors think about the AfCFTA as an investment thesis?

Institutional investors should treat the AfCFTA as a market-creating framework rather than an immediate catalyst. Its economic value creation will be progressive and non-linear, accelerating as infrastructure milestones are reached, as PAPSS adoption expands, and as Rules of Origin frameworks are operationalised across key manufacturing sectors. The most effective positioning involves identifying sectors and geographies that benefit most within a 5 to 10 year horizon, selecting investment instruments appropriate to risk appetite (direct equity for highest upside, infrastructure debt for predictable returns), and building analytical monitoring capability to track implementation progress as the primary signal of investment timing.

Share this post:

Know someone who needs to see this? Share it with them!

Ready to explore opportunities in one of Africa’s fastest-growing markets?

Investment

Opportunities in

Africa in 2026

We provide expert guidance on market entry, due diligence, and business development support.