Financing the AfCFTA

The Role of Infrastructure Bonds and Domestic Pension Funds

Updated March 28, 2026

The promise of the AfCFTA is straightforward and immense. A continent of 1.4 billion people, currently conducting only 15 to 18 percent of its trade internally compared to 60 to 70 percent for Europe and Asia, liberalises barriers to intra-African commerce and creates the conditions for the industrial development, supply chain integration, and consumer market growth that has underpinned economic transformation elsewhere in the world. The United Nations Economic Commission for Africa projects that full AfCFTA implementation could increase intra-African trade by over 50 percent and lift tens of millions of people out of poverty by 2035.

The gap between that promise and its realisation is almost entirely a physical infrastructure problem. African countries cannot trade freely with each other if the roads connecting their markets are impassable in the rainy season, if railway networks stop at national borders, if port turnaround times add two weeks to delivery schedules, or if power grids cannot maintain the reliable electricity that manufacturing supply chains require. Removing tariffs on paper is the easy part. Building the physical connective tissue of a continental market is the hard part, and it costs money that African governments, already managing constrained fiscal positions and heavy existing debt loads, do not have at the scale required.

The financing answer that is emerging, gradually but with accelerating credibility, is not to wait for more foreign aid or offshore capital. It is to mobilise the trillion dollars of African pension capital that is currently sitting in domestic bond markets and equities at sub-optimal risk-adjusted returns, and direct it toward the infrastructure assets that will generate the economic growth those pension beneficiaries’ retirements depend on.

KEY TAKEAWAYS

- The African Development Bank estimates the AfCFTA infrastructure financing gap at USD 130 to USD 170 billion annually, covering roads, railways, ports, energy interconnectors, and digital connectivity required to make intra-African trade physically viable at the scale the agreement envisions.

- Africa’s domestic pension funds collectively manage over USD 1 trillion in assets, with the South African Government Employees Pension Fund alone managing over USD 130 billion, yet the proportion of African pension capital currently allocated to African infrastructure projects is estimated at less than 5 percent of total assets.

- Infrastructure bonds issued at the sovereign or project level, when structured with appropriate credit enhancement from multilateral guarantees and domestic currency denomination, can match the risk-return and duration requirements of African pension funds in ways that conventional offshore infrastructure investment cannot.

- The AfCFTA Secretariat’s Guided Trade Initiative and the Adjustment Facility for revenue-constrained member states are creating the policy architecture within which infrastructure financing instruments can be designed with greater certainty about trade volume projections and government payment commitments.

- The most significant structural barrier to mobilising domestic pension capital for African infrastructure is not the availability of capital but the absence of appropriately structured, sufficiently rated, and domestically denominated investment instruments that pension fund trustees can hold within their regulatory mandates.

DEFINITION

The African Continental Free Trade Area (AfCFTA) is a continental trade agreement, operational since January 2021, that aims to create a single market for goods and services across 54 African Union member states, covering a combined GDP of approximately USD 3.4 trillion and a population exceeding 1.4 billion people. Its core objectives include eliminating tariffs on 90 percent of intra-African trade, harmonising trade rules and standards, and liberalising services trade across the continent.

Infrastructure bonds are fixed-income debt instruments issued by governments, development finance institutions, or special purpose vehicles to finance specific long-term infrastructure assets, repaid from project revenues, tax flows, or sovereign balance sheets over extended maturities of 15 to 30 years.

Domestic pension funds are institutionally managed pools of retirement savings capital held on behalf of working populations in African countries, currently estimated at over USD 1 trillion in aggregate assets under management across the continent, representing the largest and most rapidly growing pool of long-duration domestic capital available for infrastructure investment.

Table of Content

Financing the AfCFTA

This article is in BOH Infrastructure’s Infrastructure and Trade Corridors series. The full series establishes that physical connectivity is the single largest multiplier of AfCFTA value, and that the perception of African infrastructure risk consistently overstates the actual execution record. This briefing focuses on the specific corridors, port assets, and financing instruments that are closing the gap between ambition and delivery.

The Infrastructure Financing Gap

Anatomy and Scale

The USD 130 to USD 170 billion annual infrastructure financing gap estimated by the African Development Bank is not a single unified shortfall but a composite of multiple distinct infrastructure categories, each with its own financing logic, risk profile, and institutional complexity.

Transport infrastructure, comprising roads, railways, bridges, and border crossing facilities, represents the largest single category. The AfCFTA’s trade corridor agenda identifies specific priority corridors, including the Lobito Corridor, the Abidjan-Lagos Corridor, the Northern Corridor connecting Mombasa to Uganda, Rwanda, and the DRC, and the Trans-Saharan Highway network, that collectively require investment of several hundred billion dollars to reach the standard required for efficient intra-African commercial transport. Many of these corridors cross multiple national jurisdictions, creating the multilateral financing complexity that has historically slowed progress: a road that is excellent in one country but impassable in a neighbouring one defeats the purpose of the corridor investment entirely.

Energy interconnection infrastructure, linking national power grids into regional pools capable of trading electricity across borders, is the second major category. The Southern African Power Pool, the East African Power Pool, and the West African Power Pool each have interconnection infrastructure investment pipelines that are essential for the energy price convergence and supply reliability that AfCFTA manufacturing growth requires. The green energy transition adds urgency to this category: countries with surplus renewable generation capacity, whether Kenya’s geothermal or Namibia and Morocco’s solar and wind, can only realise the economic value of that surplus through cross-border transmission infrastructure that currently does not exist at adequate capacity.

Digital and telecommunications infrastructure, while less capital-intensive per unit than transport or energy, is increasingly recognised as the enabling layer for services trade, which is potentially the largest long-term component of intra-African economic integration. Cross-border data infrastructure, harmonised digital payment systems, and the data centre capacity to support cloud services across the continent are all AfCFTA infrastructure requirements that conventional infrastructure financing frameworks are only beginning to address.

Why Conventional Financing Has Fallen Short

The financing gap is not new information. The African Development Bank, the World Bank, and multiple development finance institutions have been publishing annual infrastructure financing gap estimates for over a decade. The gap has persisted, and in some dimensions grown, despite these estimates because the financing mechanisms that have been deployed have structural limitations that prevent them from scaling to the level required.

Official Development Assistance (ODA) from bilateral donors has been declining as a share of African infrastructure financing since 2010, and the remaining flows are constrained by donor country fiscal pressures that are unlikely to ease in the near term. Chinese infrastructure financing, which grew rapidly in the 2010s through state-backed loan structures, has slowed considerably since 2020 as several recipient countries have experienced debt sustainability concerns and as Chinese domestic economic pressures have constrained outbound lending capacity.

Multilateral development bank financing, from the African Development Bank, the World Bank Group, and regional development banks, is essential and catalytic but insufficient at current capitalisation levels to close the gap independently. The AfDB’s total lending capacity is approximately USD 10 billion annually across all sectors, a significant but small fraction of the USD 130 to 170 billion annual infrastructure need.

Offshore private capital, from international infrastructure funds, sovereign wealth funds outside Africa, and pension funds from developed countries, has historically shown limited appetite for African infrastructure at the ticket sizes and risk-return profiles that African project sponsors need. The perception of risk, as the BOH Infrastructure series has examined across multiple sectors, consistently exceeds the actual risk record of well-structured African infrastructure projects. But perception is what allocators act on, and the gap between perception and reality has not narrowed fast enough to bring offshore private capital into African infrastructure at scale.

The structural conclusion is that closing the AfCFTA infrastructure financing gap requires primarily African solutions: domestic capital mobilisation at a scale and with a sustainability that external financing sources cannot provide.

Africa’s Pension Capital

The Underdeployed Resource

The most consequential financial development on the African continent over the past two decades is not the rise of mobile money or the growth of stock exchanges. It is the accumulation of institutionally managed pension capital on a scale that now constitutes a genuine alternative to external financing for African infrastructure development.

South Africa’s pension system is the largest and most mature. The Government Employees Pension Fund (GEPF) manages over USD 130 billion in assets, making it one of the largest pension funds in the world by assets under management. The Pension Fund Administrators regulating approximately 5,000 private and public sector funds collectively manage a further USD 200 billion. Botswana’s pension system manages assets equivalent to approximately 50 percent of GDP. Nigeria’s Contributory Pension Scheme, established in 2004, has grown to over USD 30 billion in assets under management. Kenya’s NSSF and the growing private sector pension industry collectively manage over USD 12 billion. Ghana, Rwanda, Uganda, and Senegal all have formal pension systems with growing asset bases.

The aggregate estimate of USD 1 trillion in African pension assets under management understates the growth trajectory. Africa’s working-age population is the fastest-growing in the world, pension contribution rates are increasing, and the formalisation of employment in growing African economies is bringing previously excluded workers into contributory pension systems. Assets under management across African pension systems are projected to reach USD 2 trillion by 2030 and USD 4 trillion by 2040 on conservative growth assumptions.

The investment allocation of this capital is the critical issue. The majority of African pension fund assets are currently invested in domestic government bonds and listed equities, driven by regulatory requirements mandating minimum allocations to domestic assets, liquidity preferences, and the absence of suitable alternative investment instruments. Government bond yields in several African markets have been elevated relative to historical norms due to fiscal pressures, providing short-term return adequacy but creating concentration risk and limited economic development impact from pension capital deployment.

The infrastructure allocation, which should in principle be a natural match for pension capital given the long-duration, inflation-linked, and relatively predictable cash flow characteristics of infrastructure assets, is estimated at under 5 percent of total African pension assets. This underallocation is not primarily a reflection of investor preference for bonds over infrastructure. It is a reflection of the absence of appropriately structured infrastructure investment instruments that pension fund trustees can hold within their legal mandates and risk frameworks.

Infrastructure Bonds

Designing the Instrument

An infrastructure bond is not simply a government bond that happens to be associated with a road or a railway. Its design must address several specific requirements of infrastructure project financing that distinguish it from sovereign general obligation debt.

The most important design feature is the revenue waterfall: the structure that determines how project revenues are collected, what operating costs and debt service obligations are paid in what priority order, and what protections exist for bondholders in the event that revenues fall below projections. A well-structured infrastructure bond establishes a Special Purpose Vehicle (SPV) that owns the infrastructure asset, collects revenues from tolls, tariffs, or government availability payments, services the bond debt from a senior secured position in the revenue waterfall, and provides residual cash flows to equity investors. This structure insulates bondholders from the general fiscal position of the sovereign issuer and ties debt service to the specific performance of the infrastructure asset.

For African infrastructure bonds to attract pension fund investment, several additional features are typically required. Domestic currency denomination is critical: African pension funds hold liabilities in local currencies (future pension payments to domestic beneficiaries) and cannot take uncovered foreign exchange risk. An infrastructure bond denominated in USD or euros creates a currency mismatch that most African pension fund investment policies prohibit or severely restrict. The development of local currency infrastructure bond markets is therefore a prerequisite for pension fund participation, requiring deepening of domestic capital markets alongside the financing instrument design.

Credit enhancement is the second critical feature. Most African infrastructure projects, even well-structured ones with credible revenue projections and experienced operators, cannot achieve investment-grade credit ratings on their own merits at the cost of capital that makes project economics viable. Partial credit guarantees from multilateral development banks, first-loss equity tranches provided by development finance institutions, and political risk insurance from institutions such as the Multilateral Investment Guarantee Agency (MIGA) can enhance the effective credit rating of an infrastructure bond instrument to the level required for pension fund investment mandates without requiring the MDB to provide the full financing.

The AfDB’s Africa50 infrastructure fund, specifically designed to mobilise African institutional capital for African infrastructure, is the most advanced attempt to build the infrastructure finance intermediary that bridges between pension fund capital and project-level financing requirements. Africa50 raises capital from African sovereign wealth funds, central banks, and institutional investors, deploys it into infrastructure projects across the continent, and provides the fund-level diversification and professional management that individual pension funds cannot achieve through direct project investment.

The AfCFTA Policy Architecture as Financing Enabler

Infrastructure financing instruments cannot be designed in a policy vacuum. The revenue projections that underpin infrastructure bond valuations depend on credible assumptions about trade volumes, user fee collection, government payment commitments, and regulatory stability. The AfCFTA policy architecture that is progressively being put in place creates the policy foundations on which these assumptions can be made with greater confidence.

The AfCFTA Guided Trade Initiative, launched in 2022, has been building the practical trade facilitation mechanisms that translate the agreement’s legal framework into actual commercial transactions: harmonised rules of origin, standardised customs documentation, and dispute resolution procedures that give traders confidence that AfCFTA preferences will be applied consistently across signatory countries. As the Guided Trade Initiative expands from its initial pilot countries to broader participation, the trade volume projections that underpin transport corridor revenue models become more credible.

The AfCFTA Adjustment Facility, designed to compensate member states that experience short-term revenue losses from tariff reduction through AfCFTA implementation, is a mechanism that also supports infrastructure bond issuance. Governments that are compensated for revenue losses through a multilateral facility are better positioned to maintain infrastructure service payments, reducing the payment risk that infrastructure bond investors must price.

At the continental policy level, the Programme for Infrastructure Development in Africa (PIDA), administered by the African Union Commission and the AfDB, provides the prioritisation framework for cross-border infrastructure projects, designating specific corridors and energy interconnectors as continental priorities that attract multilateral attention and financing coordination. PIDA Priority Action Plan 2 (PAP2), covering the 2021 to 2030 period, identifies 69 cross-border infrastructure projects with a combined investment value of approximately USD 160 billion as continental priorities, providing a credible pipeline for infrastructure bond issuance and pension fund investment.

Turn Insight Into Action

We help investors, developers, and institutions move from ideas to bankable, de-risked projects across African markets.

Let’s turn your next investment into a structured success.

Structural Reforms Needed to Unlock Pension Capital

The mobilisation of African pension capital for AfCFTA infrastructure requires regulatory and market structure reforms in parallel with instrument design. Four specific reform areas are critical.

First, pension fund investment regulations in most African countries impose restrictive limits on alternative asset investments, including infrastructure, as a proportion of total assets. South Africa’s Regulation 28, governing retirement fund investment in alternative assets, has been progressively liberalised but still constrains the infrastructure allocation that fund trustees can make. Similar regulations in Kenya, Nigeria, and Ghana need reform to create adequate headroom for infrastructure investment without compromising fiduciary obligations to pension beneficiaries.

Second, domestic capital markets need deepening to support the liquidity requirements of pension fund infrastructure bond holdings. A pension fund can hold an illiquid infrastructure bond at a higher yield than a liquid government bond, but it requires the ability to sell the instrument in a secondary market if its liability profile changes. The development of secondary market infrastructure for African infrastructure bonds, through local stock exchange listings and market-making arrangements, is a prerequisite for pension fund participation at scale.

Third, credit rating infrastructure for African infrastructure projects needs development. International credit rating agencies apply methodologies developed for mature market infrastructure that systematically overstate African infrastructure risk relative to actual loss experience. African credit rating agencies and the African Peer Review Mechanism are developing more contextually appropriate rating methodologies, but their credibility and acceptance within pension fund investment mandates is still building.

Fourth, pan-African pension fund collaboration structures, allowing multiple national pension funds to co-invest in cross-border infrastructure projects through jointly managed vehicles, are needed to address the ticket size problem: individual national pension funds may be too small to anchor a cross-border infrastructure bond issuance, but a coalition of five to ten African pension funds acting through a shared investment vehicle can reach the scale required.

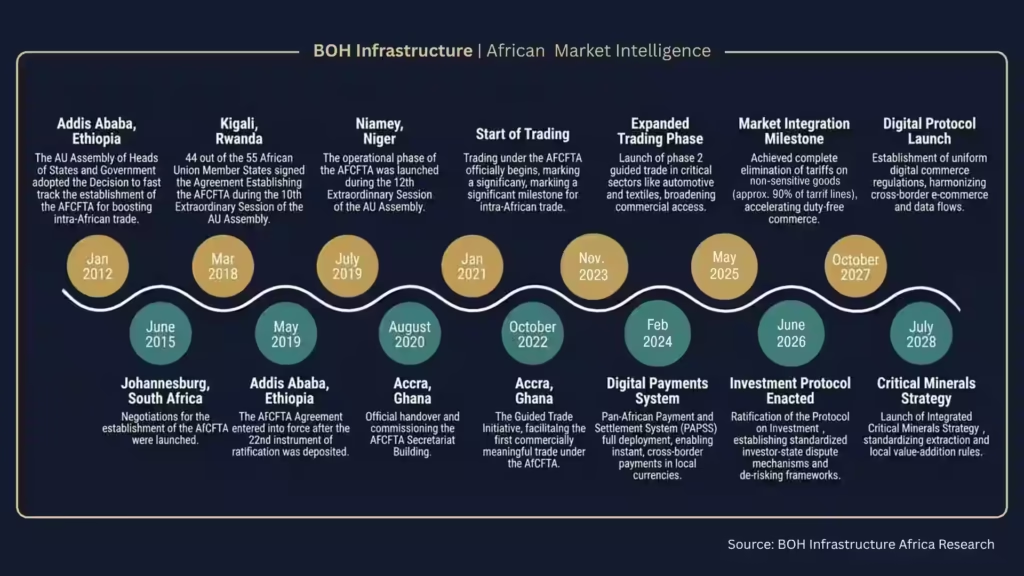

This consecutive timeline maps the evolution of the African Continental Free Trade Area from its foundational legal signatures in 2012 to its projected maturity in 2028. For institutional investors, this trajectory represents a systematic lowering of cross-border counterparty risk. The milestones forecasted for 2026 through 2028 signify transition points where isolated national projects begin to scale into bankable, continent-wide industrial assets. Source: BOH Infrastructure Africa Research.

Read → The Future of AfCFTA: Implementation Timelines for Investors

The Road from Vision to Funded Project

The journey from the AfCFTA’s infrastructure ambition to funded, construction-ready projects requires converting the enabling conditions described above into specific transactions. This is the work of the next five years, and the institutions doing it include the AfDB, Africa50, the AfCFTA Secretariat, national development finance institutions, and a growing cohort of African infrastructure advisory firms that are building the transaction structuring capability the continent needs.

For institutional investors, the emerging opportunity is to participate in the first wave of AfCFTA-linked infrastructure bonds as these instruments reach market. The first issuances will likely be sovereign-guaranteed instruments at the national level, financing specific corridor road or energy interconnection projects with clear revenue or availability payment structures. As the market develops and track records accumulate, project-level bonds with credit enhancement rather than full sovereign guarantees will follow, offering higher yields for investors willing to take on project-specific risk.

The investors best positioned to capture this opportunity are those who begin building the analytical capability, relationship infrastructure, and investment framework for African domestic currency infrastructure bonds now, before the instruments are fully developed and the market is competitive. The due diligence requirements, regulatory navigation, and local market relationship development needed to invest effectively in this asset class take time to build and represent a durable competitive advantage for early movers.

This article is part of Infrastructure and Trade Corridors series. The full series establishes that physical connectivity is the single largest multiplier of AfCFTA value, and that the perception of African infrastructure risk consistently overstates the actual execution record. This briefing focuses on the specific corridors, port assets, and financing instruments that are closing the gap between ambition and delivery. Read the full Infrastructure and Trade Corridors series.

Within this series:

- Lobito port is the western anchor of the Lobito Corridor and its development mirrors the modernisation challenges examined here. The operational standards being set at Tanger Med provide the benchmark that Lobito’s development programme is being designed to approach. → Read The Lobito Corridor: Reimagining Central African Logistics

- Mombasa’s port digitalisation ambitions are directly linked to the cost and reliability of Kenya’s national grid as cold-chain and automated port logistics scale up. → Read Port Modernization: Lessons from Tanger Med and Mombasa in 2026

Related Articles

- Green hydrogen project financing uses the same blended capital architecture described here: DFI concessional debt, sovereign equity, and export credit agency guarantees layered to bring overall cost of capital to commercially viable levels. The financing models being pioneered in green hydrogen are directly transferable to AfCFTA transport and energy infrastructure.→ Read The Rise of Green Hydrogen in Namibia and Morocco: Africa’s New Export Frontier

- Regional energy interconnection infrastructure, essential for AfCFTA energy integration, requires the same long-duration financing instruments as transport corridors. Domestic pension capital is as relevant to energy interconnection bonds as to road and rail corridor bonds. → Read Battery Storage and Grid Resilience: Solving the Intermittency Gap in 2026

Have you Read?

De-risking African Infrastructure Investment

Public-Private Partnerships PPPs: The Future of Infrastructure in Emerging Markets

How the AfCFTA’s Evolving Timeline is Re-Engineering African Project Risk

What is the AfCFTA? An Executive Overview for Global Investors

Turn Insight Into Action

We help investors, developers, and institutions move from ideas to bankable, de-risked projects across African markets.

How We Support You

- Validate opportunities with on-the-ground intelligence

- Structure investments to manage risk and attract capital

- Connect you with trusted partners, financiers, and advisors

- Navigate regulatory, financial, and operational complexity

Why It Matters

Opportunities don’t fail because they lack potential, they fail because they’re not structured to succeed.

Partner with BOH Infrastructure to unlock strategic opportunities in Africa.

Let’s turn your next investment into a structured success.

FAQ: The Role of Infrastructure Bonds and Domestic Pension Funds in Financing the AfCFTA

What is the AfCFTA and why does it require large-scale infrastructure investment?

The African Continental Free Trade Area is a continental trade agreement creating a single market across 54 African nations covering 1.4 billion people. Its transformative potential depends on physical infrastructure because intra-African trade is currently constrained not primarily by tariffs but by the cost and unreliability of cross-border transport, energy, and digital connectivity. Removing trade barriers without building the physical infrastructure connecting African markets would leave the AfCFTA’s economic potential largely unrealised.

How large is the AfCFTA infrastructure financing gap and what does it cover?

The African Development Bank estimates the annual infrastructure financing gap at USD 130 to USD 170 billion, covering transport corridors (roads, railways, bridges, border crossings), energy interconnection infrastructure linking regional power pools, and digital and telecommunications infrastructure. The gap represents the difference between what is needed to support AfCFTA trade growth and what is currently being financed through all existing public and private sources combined.

Why are African domestic pension funds considered a key financing source for AfCFTA infrastructure?

African pension funds collectively manage over USD 1 trillion in assets with a growth trajectory toward USD 4 trillion by 2040. Infrastructure assets are a natural match for pension fund capital: both require long investment horizons, infrastructure revenues are often inflation-linked, and the cash flow predictability of infrastructure assets matches pension funds’ need for reliable income to meet future benefit payments. The current underallocation of African pension capital to African infrastructure, estimated at under 5 percent of total assets, represents both a financing gap and a significant portfolio optimisation opportunity for pension fund managers.

What is an infrastructure bond and how does it differ from a conventional government bond?

An infrastructure bond is a fixed-income instrument issued to finance a specific infrastructure asset, with debt service typically tied to the revenues or availability payments generated by that asset rather than to the general fiscal position of the sovereign issuer. Key design features include a Special Purpose Vehicle structure isolating project revenues from general government finances, a senior secured position for bondholders in the project revenue waterfall, and credit enhancement mechanisms from multilateral guarantors that bring the instrument to investment-grade rating standards required by pension fund investment mandates.

What role do multilateral development banks play in AfCFTA infrastructure financing?

Multilateral development banks including the African Development Bank, the World Bank Group, and regional development banks play a catalytic rather than primary financing role. They provide partial credit guarantees that enhance the credit rating of infrastructure bonds to investment-grade levels, first-loss equity tranches that absorb initial project risk and protect senior debt holders, technical assistance for project preparation and transaction structuring, and policy coordination across multiple national governments for cross-border corridor projects. Their concessional capital is the credit enhancement layer that makes the broader financing architecture viable, not the primary source of project funding.

What regulatory changes are needed to allow African pension funds to invest more in infrastructure?

The most important regulatory changes are: liberalisation of alternative asset investment limits in pension fund regulations to increase the headroom for infrastructure allocations; development of secondary market infrastructure for African infrastructure bonds to address pension fund liquidity requirements; adoption of contextually appropriate credit rating methodologies for African infrastructure that reflect actual risk experience rather than methodologies developed for mature markets; and creation of pan-African co-investment vehicles that allow multiple national pension funds to jointly anchor cross-border infrastructure bond issuances at the required scale.

Which African institutions are most actively developing AfCFTA infrastructure financing instruments?

The African Development Bank and its Africa50 infrastructure fund are the leading institutions developing the intermediary structures and financing instruments for AfCFTA infrastructure. The AfCFTA Secretariat is building the trade policy architecture that underpins infrastructure revenue projections. National development finance institutions in South Africa, Nigeria, Kenya, and Egypt are developing domestic currency infrastructure bond programmes. The African Export-Import Bank (Afreximbank) is providing trade finance and project finance instruments that bridge between AfCFTA trade objectives and infrastructure financing requirements.

Share this post:

Know someone who needs to see this? Share it with them!

Ready to explore opportunities in one of Africa’s fastest-growing markets?

Investment

Opportunities in

Africa in 2026

We provide expert guidance on market entry, due diligence, and business development support.